Reduce Retirement Taxes with Cash Value Life Insurance

5/7/20253 min read

Why LIFT (Life Insurance as a Financial Tool) might be the missing piece in your retirement strategy.

When we think about retirement planning, we usually zero in on building a solid nest egg - stashing money in a 401(k), an IRA, or maybe even an annuity. And that’s great. After all, those accounts help you save on taxes now and grow your money over time.

But here’s what most people don’t find out until later: you’ll still have to pay taxes on that money when you start taking it out. And those taxes can really add up.

That’s where a little-known strategy called LIFT (short for Life Insurance as a Financial Tool) comes in. It’s a smart way to pre-fund the taxes you’ll owe in retirement - and even create a pool of tax-free money you can tap into when you need it most.

The Tax Trap Nobody Talks About

Let’s say you’ve done everything right — contributed to your 401(k), maxed out your IRA, maybe even built up a nice pension or annuity. The only catch? When it’s time to take that money out, the government wants its cut.

And because these distributions are taxed as ordinary income, your tax bill could be higher than you expected — especially if tax rates go up in the future.

Even worse, there are limits on how much you can contribute to those accounts each year, which means you might not be saving as much as you really need for the long haul.

Here’s Where Life Insurance Steps In

Most people think of life insurance as something you buy just in case you pass away unexpectedly. And yes, that’s a big part of it — but certain types of policies (like permanent life insurance) come with living benefits, too.

With the right kind of policy, you can build cash value over time - money you can access later on, often tax-free. That cash value can act like a safety net for retirement expenses, emergency costs, or - you guessed it - to pay the taxes on your retirement withdrawals.

This is the heart of the LIFT strategy:

Use your life insurance cash value in retirement to cover the taxes on your 401(k) or IRA distributions

Keep more of your retirement money instead of losing a chunk to taxes

Still leave behind a tax-free death benefit for your loved ones

Let’s Make It Real: A Quick Example

Say you’re retired and you withdraw $40,000 from your 401(k). Depending on your tax bracket, you could owe 20–25% of that in taxes - which is $8,000–$10,000 gone before it even hits your bank account.

But what if you used the cash value from your life insurance policy to cover that tax bill? Suddenly, you’re keeping more of your money and lowering the overall tax burden on your retirement income.

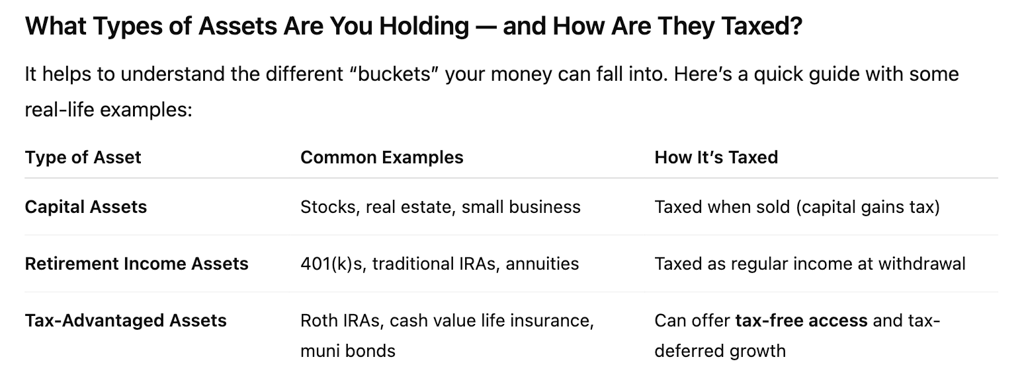

What Types of Assets Are You Holding - and How Are They Taxed?

It helps to understand the different “buckets” your money can fall into. Here’s a quick guide with some real-life examples:

Bottom line: not all income is created equal. Tax-advantaged assets give you flexibility and help reduce the risk of rising taxes eating into your retirement.

Is the LIFT Strategy Right for You?

If you're already thinking about how to protect your retirement income, fund your lifestyle, and still leave something behind for your family, then this type of strategy using cash value life insurance might be worth exploring.

Now, let’s be honest - cash value life insurance sometimes gets a bad rap. And that’s often because of policies that were poorly designed, underfunded, or misunderstood. But when structured and funded properly, these policies can offer significant long-term benefits:

Tax-free growth

Tax-free access to cash value (living benefits)

A tax-free death benefit

Flexible income for retirement or emergencies

In short, it’s not about the product itself - it’s about how you use it as part of a bigger plan.

You might benefit from this approach if:

You want more control over your retirement taxes

You're ready to properly fund your policy

You’re looking for tax-free income options in retirement

Final Thoughts

Look - life insurance isn’t just about planning for the worst. It can also be a powerful financial tool for planning the best: a retirement where you have more control, fewer tax surprises, and a bigger cushion when life happens.

If the idea of paying less in retirement taxes sounds good to you, let’s talk. I can help you figure out if a policy like this fits into your overall plan - and show you how it might help you keep more of what you’ve worked so hard to earn.

Let’s Connect

Want to learn more about how life insurance can work for you while you’re still living?

Reach out today for a no-pressure conversation

Victor Ortega

A reliable partner in Temecula, CA Victor Ortega offers health insurance plans for individuals, families and small groups. As well as life, Medicare, and supplemental.

vic@vicinsurescali.com

© 2026. All rights reserved.

Licensed Insurance Agent License #4424316

This website is owned and maintained by Victor Ortega, which is solely responsible for its content. This site is not maintained by or affiliated with Covered California, and Covered California bears no responsibility for its content. The e-mail addresses and telephone number that appears throughout this site belong to Victor Ortega and cannot be used to contact Covered California.